Risk & Compliance

Making machines learn compliance

Firms are tapping ML and AI to detect ‘false positives’ to limit non-compliance failures.

Organizations are implementing new stress testing models to gauge investment risk and meet regulatory compliances — a challenge heightened by the coronavirus pandemic. This has led to increased investments in data sciences and automation solutions, thereby cutting costs incurred due to compliance failures.

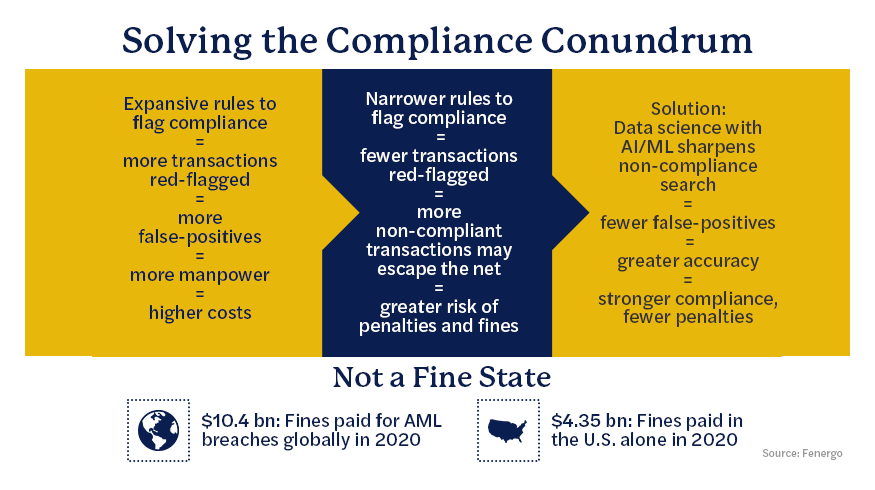

There is a classic dichotomy in the area of compliance. On the one hand, a company needs to identify areas of non-compliance. In the process, on the other hand, it might end up finding a plethora of transactions that need to be investigated for non-compliance, and spend most of its energy, time and money in investigating false positives.

As companies install more regulations to identify more potential risks, the number of false positives increases manifold. In order to mitigate this problem, organizations have begun to invest significantly in data sciences services and in machine learning and artificial intelligence. This, they hope, will reduce the number of false positives and enable them to identify non-compliance with greater accuracy.

Companies are investing also in anti-money laundering (AML) solutions, which form a large part of the compliance exercise, and for good reason. Failing to detect fraud or money laundering activities can get companies on the wrong side of regulators. Globally in 2019, fines worth $8.14 billion were levied for AML-related breaches; U.S. regulators alone imposed $2.29 billion of those fines.